In subrogated motor claims, a familiar exchange often occurs during the discovery process.

An insurer produces an engineer or assessor report identifying the reasonable cost of repairing accident damage. The defence then responds with a request for further documents, typically including:

-

proof that the repairs were actually carried out

-

the repair invoice

-

proof that the policyholder paid their excess.

The implicit suggestion is that, without these documents, the claim for repair costs cannot succeed.

As a matter of law, that suggestion is incorrect.

The Legal Loss Is the Damage to the Vehicle

The starting point is the orthodox principle governing damage to property.

In our previous article we explored the principle of Restitution Ad Integrum in the context of motor damage claims.

We clarified that when negligent driving damages a vehicle, the Plaintiff’s loss is the diminution in the value of the vehicle caused by the accident.

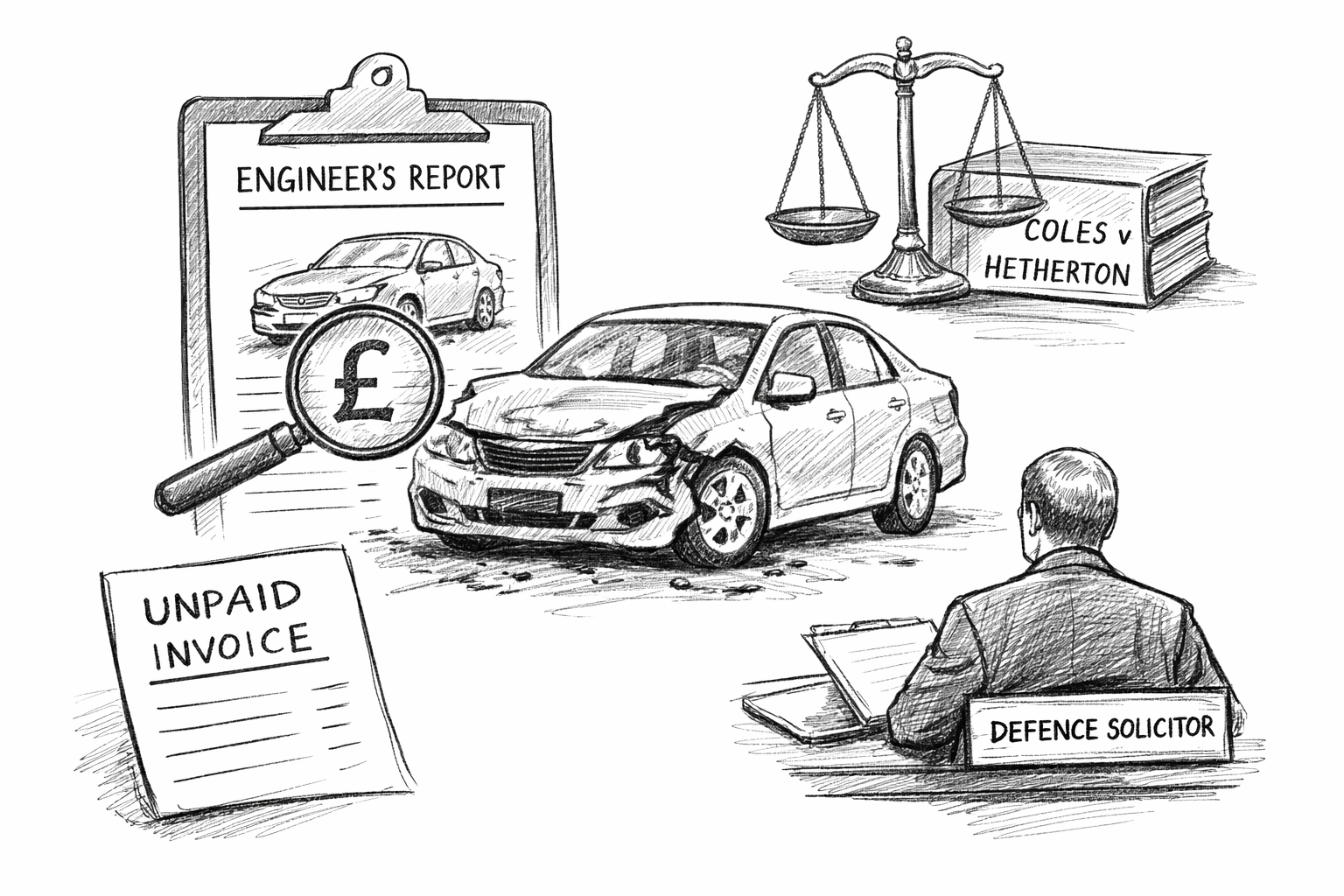

The Court of Appeal explained this clearly in Coles v Hetherton, stating:

the reasonable cost of repair is only a way of ascertaining the diminution in the value of the chattel by reason of the physical damage.

This passage identifies the crucial analytical point.

The repair cost is not the loss itself. Instead, it is simply the usual way in which the courts measure the reduction in value caused by the accident.

The loss arises at the moment the vehicle is physically damaged in the collision.

Repairs Are Not a Precondition to Recovery

The Court of Appeal in Coles v Hetherton also addressed the evidential question directly.

The court confirmed that the reasonable cost of repair may be assessed:

whether or not repairs have been done and whether or not an invoice is produced.

This reflects the underlying logic of the law.

If the Plaintiff’s loss is the diminution in value caused by the accident, it cannot logically depend on whether the plaintiff later chooses to repair the vehicle.

Vehicles are frequently:

-

sold unrepaired

-

written off

-

repaired privately

-

repaired at a later date.

In all of these scenarios, the loss caused by the accident still exists.

Accordingly, courts routinely assess vehicle damage using evidence such as:

-

engineer or assessor reports

-

repair estimates

-

expert evidence on repair methodology

-

valuation evidence.

What the Plaintiff Must Actually Prove

Although repairs are not required, the Planitiff must still prove the amount of the loss.

In practice this usually requires evidence establishing that:

-

the vehicle was repairable

-

the proposed repairs were reasonable and necessary

-

the claimed figure represents the reasonable cost of repair.

An independent engineer or assessor report will often provide precisely that evidence.

What the law requires is proof of the reasonable cost of repair, not proof that the repairs were actually carried out.

What About the Policy Excess?

In subrogated claims, defence solicitors sometimes also request proof that the Policyholder paid their policy excess to the insurer.

This request generally arises because the claim is being pursued by the insurer exercising rights of subrogation.

However, the legal analysis remains unchanged.

Subrogation simply allows the insurer to exercise the insured’s cause of action against the wrongdoer.

The measure of damages remains the same: the loss caused by the accident.

Whether the insured paid their excess is therefore primarily a matter between insurer and insured, rather than a prerequisite to establishing the defendant’s liability for the vehicle damage.

Why These Requests Arise in Practice

Requests for proof of repair are usually not based on the legal measure of damages.

More commonly, they reflect a forensic concern about the reasonableness of the claimed repair cost.

For example, the defence may wish to test:

-

whether the repair estimate reflects real market repair costs

-

whether the repair methodology is appropriate

-

whether the estimate includes unnecessary work.

Those are legitimate issues. But they go to the reasonableness of the repair cost, not to whether repairs were carried out.

The Real Litigation Point

A Plaintiff does not need to prove that repairs were carried out in order to recover damages for vehicle damage.

What must be proved is the reasonable cost of repairing the accident damage, which is simply the conventional way of quantifying the diminution in value of the vehicle.

An engineer’s or assessor’s report may be sufficient evidence of that figure.

Requests for repair invoices or proof that the policy excess was paid do not alter the fundamental legal principle confirmed in Coles v Hetherton.

Why This Matters for Subrogated Motor Claims

Subrogated claims frequently involve disputes over relatively modest property damage.

In that context, defence requests for additional documentation can sometimes risk obscuring the real legal issue.

The court’s task is not to determine whether repairs were carried out, but rather:

What is the reasonable cost of repairing the damage caused by the accident?

Where that question is answered by credible engineering evidence, the absence of a repair invoice does not prevent the court from assessing the claimant’s loss.

For practitioners handling motor damage claims, the lesson from Coles v Hetherton is straightforward: the law compensates the damage to the vehicle, not the repair invoice